Poland's asset management industry saw stable growth across all but one segment in H1 2014. Assets of regulated investment funds and assets in voluntary pension plans - pillar III kept growing quickly and reached PLN 203 billion and PLN 15 billion, respectively. Also managed funds* of insurance companies showed positive development climbing to PLN 152 billion, as of H1 2014. In contrast, Pillar II assets plunged by nearly 50% to PLN 152 billion as the overhaul of the second-pillar pension system, in early 2014, resulted in a forced transfer of roughly half of segment's assets to the state-run social security institution. As a consequence, despite positive developments in most segments, the total value of assets under management (AuM) in Poland contracted to PLN 522 billion (€ 124 billion) in H1 2014. Three large firms: PZU, Aviva and ING remained the key asset managers in the country with a combined value of AuM of over PLN 200 billion. However, most of major asset managers continued to lose market share in favor of smaller and more flexible specialists, growing quickly in market niches.

Outlook The asset management industry in Poland is expected to sustain a moderate growth of ~7% p.a. by 2016. New inflows from individual clients will fuel investment fund assets, unit-linked insurance and Pillar III pension plans. One of factors supporting new investments will be exceptionally low market interest rates which are backing up the process of bank deposits conversion. However, the most important growth factor will be constantly increasing wealth of individuals, which has persisted for over 10 last years. The institutional part of asset management business is also likely to expand in the future although at slower rates than the retail segment. As far as the profitability of asset managers is concerned, Inteliace Research expects that the pressure on margins will intensify inline with the growing number of competing asset managers operating in the market, which eventually will lead to market consolidation around the most efficient players.

* Technical reserves of non-life and life insurers, including unit-linked life funds.

2. Asset Management Market

Slide 1: Asset management market in Poland – Key Segments, 2014 H1

Slide 2: Assets under management evolution, 2009–2014 H1

Slide 3: Top asset managers (groups) by AuM, 2014 H1

3. Investment Funds

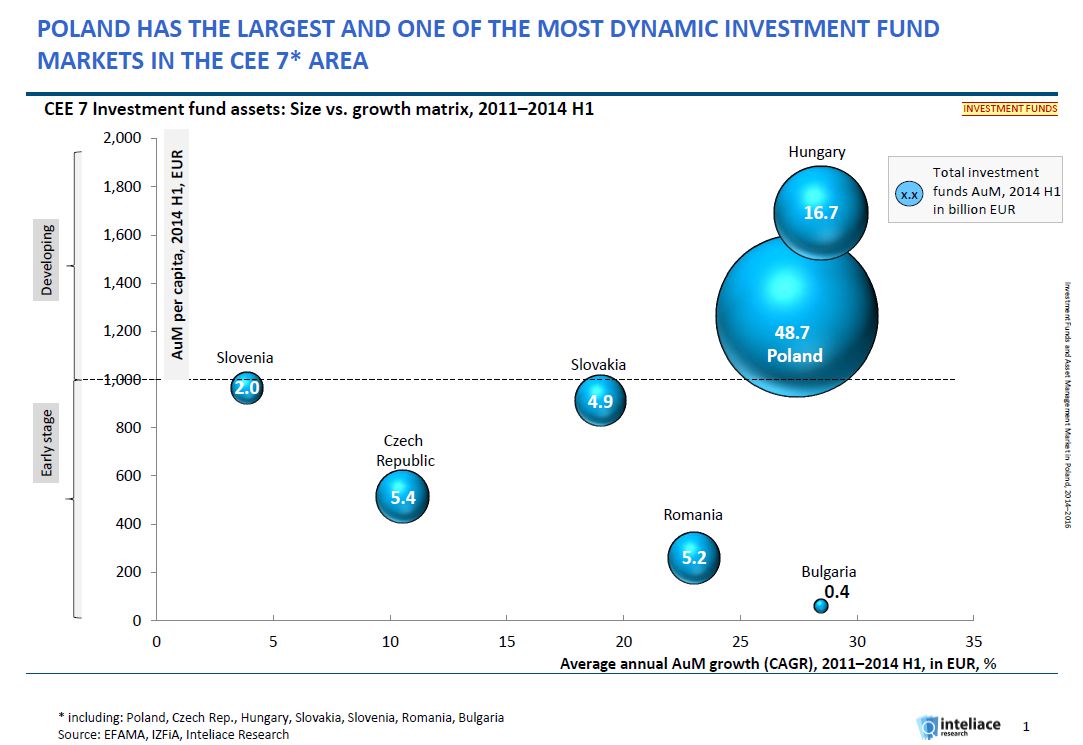

Slide 4: CEE 7* Investment fund industry - size vs. growth matrix, 2011-2014 H1

Slide 5: CEE investment funds penetration benchmarks, 2014 H1

Slide 6: Evolution of assets, number of funds & managers 2009–2013 (2014 H1)

Slide 7: Fund assets by type of fund, 2010-2013

Slide 8: Top players in investment fund market, 2014 H1

Slide 9: Market share evolution of top fund managers, 2009-2014 H1

Slide 10: Distribution channels for investment funds, 2014 H1

Slide 11: Investment fund assets flows, 1Q 2009–2Q 2014

Slide 12: Fund assets structure, 2014 H1

Slide 13: Ownership of funds by groups (retail/financial/other), 2009–2014 H1

Slide 14: Local funds invested in foreign assets and foreign funds, 2014 H1

Slide 15: Assets of foreign funds, 2009-2014 H1

Slide 16: Fees and commissions charged by top fund managers, 2014 H1

Slide 17: Revenues and costs of fund managers, 2014 H1

Slide 18: Profitability tree for fund managers, 2010–2013

Slide 19: Top players’ profiles - PZU TFI

Slide 20: Top players’ profiles - Ipopema TFI

Slide 21: Top players’ profiles - Pioneer Pekao TFI

Slide 22: Top players’ profiles - PKO TFI

Slide 23: Top players’ profiles - Skabiec TFI

Slide 24: M&A transactions including fund managers in Poland (1/2)

Slide 25: M&A transactions including fund managers in Poland (2/2)

Slide 26: Recent case examples of entry of foreign fund managers to Poland

5. Insurance

Slide 33: Insurance assets by type evolution, 2009-2014 H1

Slide 34: Profitability of life insurers, 2010-2013

Slide 35: Profitability of non-life insurers, 2010-2013

Investment funds and asset management market in Poland, 2014

Investment funds and asset management market in Poland, 2014